New renewables are liberal coded 💅: part three - Outlook and shortcomings

Why renewables are inherently liberal and strengthening the role of liberalism globally

This is the final blog of a three part series arguing that renewables are inherently liberal. For full context, we advise you read part one on equipment (here) and part two on electricity markets (here).

What does the future hold?

The growth of renewables will continue for quite some time before reaching its limits. Across BNEF and IEA forecasts for 2035 we’ll be reaching >50% share of renewables in electricity. 2050 will see largely renewables-driven energy systems.

Gaining ground

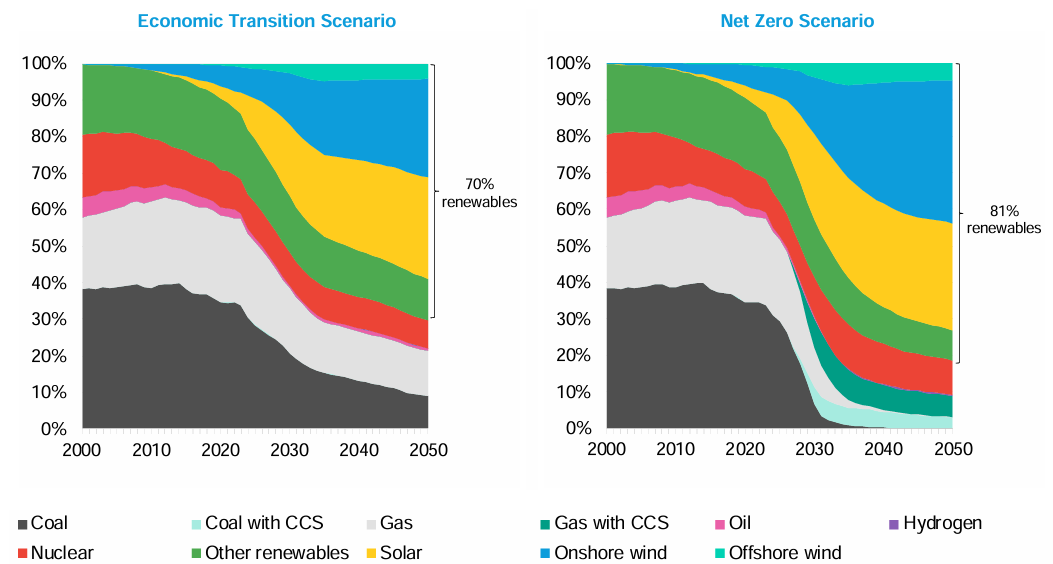

In any scenario, renewables are set to dominate the global generation mix.

Source: BNEF World Energy Outlook 2024

Source: IEA World Energy Outlook 2024

For the coming decades, we believe this could lead to:

A) liberalisation at a higher, global level, but

B) intervention needed in areas where markets fail.

A | How could renewables strengthen the trend towards liberal societies globally?

Overall, it’s a shift in power from rent seekers to the rest of us:

Decoupling from rent seekers: First, it will decouple liberal societies from petro-states and without the threat of cutting people off from fossils, e.g. Putin will wield less power over Europe. Policies such as REPowerEU or the Inflation Reduction Act accelerate domestic energy production.

Decline of rent seekers: Second, it will lead to a decline in power of illiberal countries backed by resource extraction. Putin relies on oil and gas revenues to keep his war machine going but also to suppress his own people. Cutting off that revenue stream means this power will crumble and hopefully a transition to a proper democracy can begin.

Stabilisation: Lastly, an abundance in energy decoupled from global markets and its deflationary impact could alleviate poverty in poorer nations, reduce financial dependence on others and hence reduce migration and conflict.

B | Where does the market fail and liberalism fall short?

Inconsistent carbon pricing: Price all carbon. Put a fence around the market (such as the Carbon Border Adjustment Mechanism). Distribute the revenues raised to consumers. Simple. This will accelerate a transition to renewables, with high emitters paying penalties and low emitters receiving support. Market participants aren’t disadvantaged and emissions aren’t simply offshored.

Market distortion: Subsidies are an important lever for incubating and accelerating the development of emerging technologies. However, once mature, they should not benefit investors at the expense of society. Fixed payments per unit of electricity have led to ongoing negative pricing, highlighting the need for a more effective approach. Implementing consistent carbon pricing and allowing market forces to operate freely would be ideal, but we do recognise this may be wishful thinking. Instead, regulators should aim to design subsidies that are market-efficient (such as CfDs with a kock out at price < 0) and prioritise eliminating other barriers to buildout, such as minimum distance requirements and or lengthy approval processes.

Winter supply and backup: Insurance type events are easily mispriced. Raising capital for an unlikely but crazy high payoff is a tough one, while always at risk of governments capping your returns with some fairness or windfall tax. Hence, for a society it is probably easier and better to pay for an insurance premium, such as the British capacity markets do (fight a market failure with another market!). Generally, policy makers are aware of this problem, but it looks like many will just keep fossil plants on standby as sufficient support is missing for a clean alternative, such as hydrogen and carbon capture and storage (CCS). This is essentially a special case of the missing money problem. The general case of bulk energy generation, we do not see as a particular issue in a market with proper carbon pricing and without buildout restrictions.

Unreasonable risk taking: As the UK deregulated energy supply, a bunch of small shops popped up, offering dirt cheap rates. Partly due to license fees being pocket change so any team with laptops could open a business in a garage and undercut competition on operating cost. However, also due to the lack of regulation to actually procure energy and hedge long term exposure, suppliers sold you energy for the next year and kept an open short exposure. Now, if prices at least stay steady, they make a sales margin without the cost of hedging. If prices rise, well, the suppliers go bust and the customer could run dry. Debundling led to fierce competition which is generally good for consumers, but regulators must clearly set a framework laying out what risks suppliers can and cannot take, similar to banks.

Stranded consumers: As gas consumption falls, fixed costs of grids need to be rolled over to fewer consumers, whose bills rise, enticing them to switch to heat pumps. This reinforces the trend until only those are left who cannot afford to switch. Grandma now sits on an old gas boiler without access to gas. Hence, financing support or backstop must be given to protect them. Some utilities are starting this communication early to enable a transition over many years.

The transition is well underway and market forces are practically unstoppable at this point. Much more needs to be done to address these shortcomings before they become systematic problems. But if we steer our system the right way, we’re looking at an era of abundant, clean energy, halting further climate change and hopefully stabilising nations, supporting a peaceful and prosperous life for everyone.